Related party transactions and transfer pricing in Vietnam

Hi DMS Attorney in Vietnam! Enterprises, individuals may buy shares, shares of capital contribution in some other companies. These companies have purchase goods, services with each other. Can you advise me about related parties, related party transactions, transfer pricing ?

Hi!

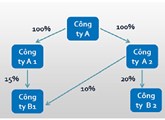

“Related-party transactions” are transactions arising between parties having related-party relationships (Clause 22 Article 3 Law on Tax Administration No. 38/2019/QH14 dated 06/13/2019).

Related parties are parties participate directly or indirectly in the management, control or capital contribution of an enterprise; parties are put under the common management, control of an organization or individual directly or indirectly; parties receive capital contribution by the same organization or individual; enterprises are managed, controlled by people who have close relationships in the same family (Clause 21 Article Law on Tax Administration No. 38/2019/QH14 dated 06/13/2019).

Specific provisions to determine related parties are mentioned in Article 5 Decree No.20/2017/ND-CP dated 02/24/2017 prescribing tax administration for enterprises engaging in related party transactions.

Taxpayers engaged in related party transactions shall be held responsible for preparing, retaining, declaring, providing dossier for information about the taxpayer, taxpayer’s related-parties including information about related parties reside in other countries, territories outside of Vietnam according to the Government’s regulations (Clause 13 Article 17 Law on Tax Administration No. 38/2019/QH14 dated 06/13/2019).

Principles for declaration, determination of taxable price of related party transactions are as follows:

Declaring, determining prices of related party transactions (transfer pricing) on the principle of analysis, comparison with independent transactions and the principle of substance over form of transactions, activities to determine tax obligation similar to condition for transactions between independent parties;

Related party transactions are adjusted according to comparable independent transactions to declare, determine tax payable on the principle not to decrease the taxable income;

Small-size, low-risk taxpayers shall be exempt from implementation of regulations in Points a, b of this Clause and be entitled to apply simplifying regime in declaring, determining transfer price (transfer pricing) (Clause 5 Article 42 Law on Tax Administration No. 38/2019/QH14 dated 06/13/2019).

Related topics:

Cases exempted from declaring, preparing transfer pricing documentation

Corporate Income Tax (CIT) rates in Vietnam.

Corporate Income Tax exemption and reduction in Vietnam

Consulting services:

Phone: 0914 165 703 or email: dmslawfirm@gmail.com

Related parties and transfer pricing in Vietnam

| Prepared by: Thi-Ha Nguyen, ACCA | DMS Law firm in Vietnam Director (Signed) Lawyer Do Minh Son |

RELATING ITEMS

Can a company deduct office rents paid to an individual landlord ?

26 May, 2020// Group: LAW ON ACCOUNTING AND TAXESIn case an enterprise leases assets from an individual and there is an agreement in the lease contract that the rent is exclusive of tax

VAT for intra-company transactions between a company and a branch

26 May, 2020// Group: LAW ON ACCOUNTING AND TAXESLawyer in Vietnam advises about VAT for intra-company transactions between a company and a branch

Declaration and payment of Business license fee in Vietnam

26 May, 2020// Group: LAW ON ACCOUNTING AND TAXESExemption of business license fee in the first year of establishment or doing business (from January 01 to December 31) is applicable to

An enterprise lends out its idle cash to other organizations, individuals

26 May, 2020// Group: LAW ON ACCOUNTING AND TAXESSeparate loans that are not a business and irregularly given by taxpayers that are not credit institutions

Cases exempted from declaring, preparing transfer pricing documentation

26 May, 2020// Group: LAW ON ACCOUNTING AND TAXESA taxpayer shall be exempted from declaring, preparing the transfer pricing documentation referred to in Sections III and IV of the Form 01 given in the Appendix to this Decree only if